The content you include in your investor deck will vary slightly depending on whether it’s an angel, seed round, Series A, Series B or subsequent stages of venture capitalist fundraising. But regardless of your company’s end goal, it’s important to avoid common pitfalls that could easily make an otherwise great pitch deck fail you. Here are five slides you should ditch in your next investor pitch deck.

Don’t talk about acquisition or potential buyers too early

Of course you have been testing different acquisition sources and tracking where your users are coming from. Obviously you want to demonstrate your ability to develop long-term customer acquisition strategies and highlight which channels do and don’t work, but the common mistake many presenters make is jumping into it too early. Make sure to describe the problem first and clearly outline your value proposition. If the investor is not convinced the problem is real and your solution is both feasible and timely, any customer acquisition success will seem circumstantial, and any long-term acquisition strategies you propose are unrealistic.

Don’t worry about traction at the seed stage

Traction and product-market fit are two things that are often confused. Many companies have traction but very few have product-market fit. That’s because early traction can be a temporary or accidental success, often boosted by circumstances such as personal and industry connections of one of the founders.

On the other hand, if you manage to demonstrate that you’ve reached the stage of product-market fit, you’re showing that you’ve found your ideal target market and are developing the perfect solution to their problem.

To demonstrate proof of product-market fit, ask yourself the following questions (and make sure to include the answers in your presentation):

Do your customers recommend your product to others?

Do they bounce, and how often?

What are the key metrics for customer success (aka conversion)?

You are a start up. Traction is important, however, depending upon your stage, you need to also consider the investors, are they the correct audience? Angels, VC, PE etc. Be considerate of your time and research!

Don’t talk about financial projections without having clear comps

Many start-up founders think that they need to be aggressive in their financial projections because investors will haircut their forecast. Sure, it’s true, they will haircut your forecast. But it still has to be realistic if you want to get any funding at all. Stating that your revenue will grow from zero to $100 million in the first two years is not realistic. Be optimistic but honest. Make sure to include your upcoming expenses as well as your projected cash flow.

We realise we may believe we have a unicorn company, yet, we don’t need to be there tomorrow. Realism is your ally. If you build a business with a true growth strategy, a researched thesis as to how you’ll achieve and demonstrate “we’re going to get there, yet with capital, we’ll get there quicker and more efficiently”.

As a rule of thumb, many growth-stage investors (Series B and beyond) follow the “The Rule of 40” to assess the growth of fast growing start-ups. According to this rule, the company’s combined growth rate and profit margin should be at least 40%.

Don’t ask for a specific sum of money

Likewise, when you ask for a specific sum of money, be realistic and be willing to explain how the money is going to be used. Include answers to these questions in your presentation (or be prepared to elaborate): How much money would you like to raise? Why this amount? What exactly will you do with it and how long will it last? Be sure to mention any upcoming hires, or tools and services that you will need for your business to grow and run smoothly.

My advice is to place a bracket i.e. between $5m and $10m then discuss the definitive rationale of both.

Don’t forget to mention the team

The team behind your start-up is the soul of the company. They are just as (if not more) important than your brilliant idea. A common mistake first time entrepreneurs often make is to stop after mentioning the founder and the co-founder.

Potential investors want to know not only about the founders of the company but about the team members, too. Explain what experience and skills they bring to the table, their motivation and enthusiasm, and why they’re a valuable asset to your company.

Talk about the members of your team and any anticipated additions down the road. Briefly add what each member brings to the table, to help move the vision forward and the company grow.

As mentioned previously, you business will change direction at least once before you ‘make it’, yet with a strong team with you will allow this adaptability to be on the journey with you through this transition! The stronger you are as a unit, is defendable.

If you’re at a stage where you have the contents ready, but feel a conversation of structure, design and content, reach out and I’ll help you.

If you’ve wanted to run your own business, this is a great time to do it.

You’ve considered running a business but keep wondering whether conditions are right to support your winning idea. Or perhaps you have been dabbling with something on the side and can’t yet convince yourself that it’s the right time to take the leap from safety.

There’s always risk in starting a business. But the present is a great time to do so. Here are 10 reasons to start your next act and become an entrepreneur now.

1. Technology has become your pal.

A modern business needs technology. Even if you’re not creating the next hit app, you’ll want customer relationship management, accounting, website, and email hosting, and possibly design software, or other tools. Cloud computing lets you get needed services on a monthly basis without laying out too much cash at the start. Also, hardware is relatively cheap, so getting an upgraded PC or tablet won’t cost a body part or two.

2. Your current job isn’t a path to happiness.

Having a career is a fine goal. But placing faith in a job as a way to advance is a poor strategy. As someone recently pointed out, mediocre bosses typically get ahead in corporations, because they are the most likely to make “safe” choices. When you work for such a boss and company, you won’t get a chance to shine, either, or learn what you need to grow.

3. Entrepreneurship has been on the decline.

As researchers at the Brookings Institution have shown, entrepreneurship has been on a decline in this country for decades. The rate at which new businesses start has fallen below the rate at which they close. The reason isn’t exactly clear, but it doesn’t have to be. Fewer startups mean less competition for money, people, attention, and customers.

Even though potential competition has dropped, it hasn’t gone away. But that’s no matter, either. Competitors help create and enlarge markets, acting as a marketing multiplier and giving credibility to an endeavor. In addition, you can make competitors work for you. Welcome them.

5. You don’t have to risk it all.

Worry about risking it all is understandable, particularly if you have people who depend on your ability to bring home a paycheck. But there’s no reason to jump into the deep end of the business pool if you don’t have the resources for such a gamble. Start your business on the side. Given how so much in communications and human interaction now happens online, it’s easier than ever to get a part-time venture going, find a market, close business, and get paid.

6. You’re no longer a sitting duck.

The flip side of entrepreneurial risk is the chance you take working for a corporation. When things get bad – and they can, without any notice companies often downsize. Too often someone with more experience gets booted out the door to be replaced by someone cheaper because a bean-counter assumes that everyone is completely interchangeable. Or maybe you’ll hear that the company has reduced benefits or moved your office to another state. At least start developing your business on the side, so that you have some options if things turn sour and you become part of this season’s staff reductions.

7. Globalisation is your secret friend.

Globalisation has been brutal on millions of people who became sitting ducks when their jobs were shipped overseas. And yet, the trend does have its upside for businesses of all sizes. There are new sources of products, components, engineering, design, and other resources at lower prices than in the U.S. Also, there are new markets offer ingfresh opportunities.

8. You can find lots of help.

All those talented and experienced people who now have no jobs because they were sitting ducks have found that new job creation has mostly been in low-paying sectors. That means there are enormous personnel resources waiting for a reasonable opportunity. If you need talent, you can find it.

9. You’re on the right side of regulation.

Executives love to bemoan how regulations are “killing” them, even as profits and revenue climb every year. Yes, let the tears flow. The good thing for your startup is that it’s much smaller than the cut-off for many regulations, so you can operate more freely and agile than larger competitors. Another obstacle for entrepreneurs, the need for health insurance, can keep aspiring entrepreneurs tethered to a corporate desk.

10. Waiting won’t help

The biggest reason that now is the right time is that later almost never is. You can wait yourself into old age and regret, but you don’t need to. Even if your business doesn’t work, it won’t be the end of your life. Many entrepreneurs go through multiple businesses before they find the one that works for them. In the words of playwright Samuel Beckett: “Ever tried. Ever failed. No matter. Try Again. Fail again. Fail better.” But do it now.

Personal resources

Planning and starting a new business is a full-time job, so it’s important to ensure that you have time that you can dedicate to the process. If you’re already working, the time that goes into planning, launching and running a business – deciding on location, a marketing strategy, hiring staff, and much more! – will all be happening around your 9-5 work routine. It’s also important to consider your family commitments, as these will be affected, as you need time to dedicate to your new venture. The solution lies in planning well in advance and managing your time effectively as you transition into a business owner and entrepreneur.

Financial resources

Timing the start of a new business is a matter of risk assessment. Do you have enough startup capital in order to purchase equipment or put a down payment on a lease? Do you have the necessary funds to invest in a business long term, and what kind of return on investment are you hoping for, so that your business is profitable and can continue to invest in it? If you’re thinking about launching a company, it’s a good idea to consult a financial advisor with expertise in the startup sector, or a business set-up agency to review your business plans and help with the right budget.

Motivation

There are lots of motivators for starting a new business. You might have a great idea for a niche product or service, or you may have reached a stage in your life where you’re ready to be your own boss. Whatever the reason, it’s necessary to capitalise on your personal motivation and stay energised, and make the right business decisions that lead to a quality product or service that’s profitable.

If you’re ready – or think you are – and want some sound, impartial advice from someone who has been there several times reach out and let’s talk it through.

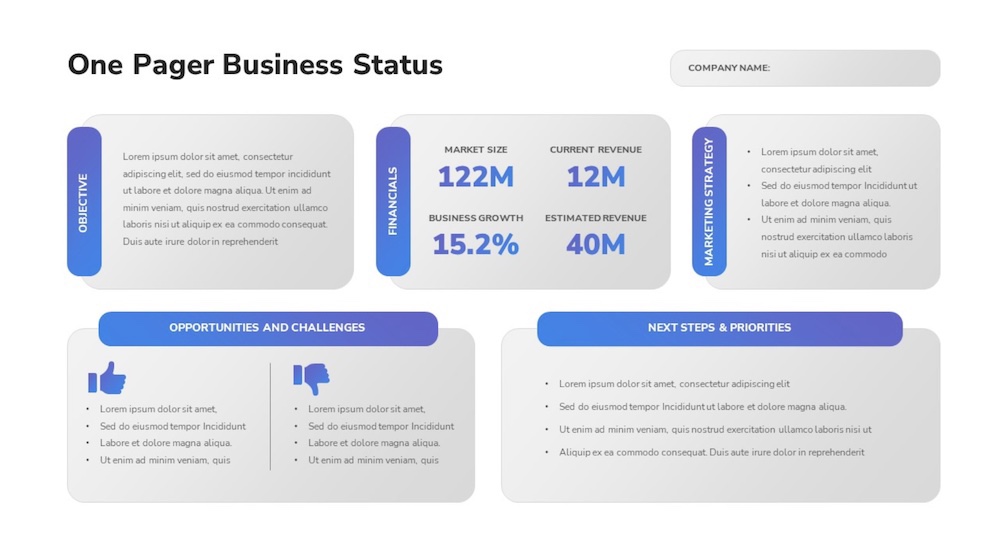

Series A, Series B, and Series C pitch deck serves as vital presentations for startups during distinct funding phases, aiming to secure investments from venture capitalists or other investors. Though their content and structure may vary, their unified goal is to captivate potential investors and propel the startup towards growth.

Series A

The Series A pitch deck is a crucial tool for budding startups in their initial growth phase, aiming to secure substantial funding after the seed stage. This presentation zeroes in on showcasing market validation, traction, and growth potential. It spotlights the startup’s product, market scope, target audience, business model, competitive edge, and early customer acquisition strategies. Despite potential limited revenue or profit for early-stage startups, the pitch deck often incorporates financial projections, essential key performance indicators (KPIs), and a roadmap illustrating how the secured funds will fuel the journey toward growth.

Series B

The Series B pitch deck becomes pivotal as startups enter a phase of maturity, actively pursuing funding to expedite growth and scale their operations. During this stage, showcasing robust growth metrics, market traction, and revenue generation potential is crucial. The pitch deck accentuates revenue projections, strategies for customer acquisition and retention, expansion blueprints, team expertise, and competitive positioning. In the financial segment, it offers a transparent view of the startup’s fiscal health, growth rates, burn rate, and prospective profitability. It emphasizes the projected return on investment, empowering potential investors to make informed decisions.

Series C

The Series C pitch deck marks a stage for well-established startups, highlighting substantial growth and ambitions to introduce fresh offerings or venture into untapped markets. This presentation accentuates the startup’s adeptness in securing a greater market share, sustaining a competitive edge, and ensuring profitable operations. It dives into discussions regarding international expansion strategies, strategic alliances, novel product innovations, and effective customer retention methodologies. At this level, the pitch deck is meticulous in presenting a well-defined roadmap to profitability, positive cash flow, and attractive exit opportunities for potential investors. It encompasses in-depth financial projections, crucial financial metrics, and a thorough valuation analysis of the company.

Grab a note pad and draw out your slides/template structure first!

After a while and thousands of iterations, your pitch deck will evolve, work on one, a thorough deck, keeping the information relevant and factual, then you can extract these pages, to make a shorter deck to the audience that requires it.

My advice, don’t send a pitch deck, send a one page summary instead. You want face time, build a relationship and you’ll avoid investing time with those who aren’t interested, but don’t want to be the one who is known for saying no to the next Uber/AirBnb!

If you need company branding advice, design and templates, let me know and I’ll support you.

While both business and job seem lucrative to respective groups of people depending on several factors, the main differentiating factor in opinion is the perception towards an income that a person maintains.

There has long been a conflict between work and business. Which of these two professional choices is best for achieving personal and financial progress is a topic on which everyone has an opinion. Both business and employment come with various benefits and drawbacks, and it might take time to decide between a job and a business.

When you pick a career, you can find work or start your own business. Each alternative has pros and cons,while the jobs vs business debate has been going for ages. Let’s analyse how they differ from one another.

How to Decide Between Jobs vs Business?

You can establish your own business or look for employment when ready to enter the workforce. Each has advantages and specific difficulties with doing a job or running a business. Finding the best choice might be aided by understanding the distinction between a job and a business.

Comparison of Jobs vs Business

An organisation or entrepreneurial entity engaging in commercial, industrial, or professional activity is what is meant by the concept of business. Businesses can be for-profit corporations or charitable institutions. Limited liability firms, sole proprietorships, corporations, and partnerships are among the several forms of businesses.

On the other hand, a job can be simply described as a piece of work, particularly a specified activity completed as part of one’s regular workday or for a fixed amount. The routine job that a person performs to make a living while dedicated to an organisation is what best describes the term.

Profit vs Salary

If you own a firm, your prospective profits are usually more significant. As a business owner, you occupy the highest position in your organisation, and your remuneration reflects this. As an employee, you can earn more based on your experience and education, but you will seldom make as much as a successful company owner. A salary is earned in a job, however, company owners can receive a salary while also enjoying the earnings of their firm when it is successful.

However, your income from a job is more consistent than your revenue from a business. When you go to work, you get compensated for your time, and you may not be able to do so if you run a firm.

Planning is a key to a successful underpinning of your new venture.

Risk Factor of Job vs Business

Working is nothing compared to owning a business. As a CEO, you will spend many years honing many talents.

You can get dismissed from a job and still find work, or you might lose your company overnight, making establishing a new company or looking for work a nightmare. In terms of risk, a job is preferable to a business.

Qualifications needed for Job vs Business

Being a business owner does not need any special credentials. There are several methods for learning how to establish a business. You can get a business management degree, learn from a mentor, self-teach, or hire a business counsellor. As a company owner, you may set your qualifying criteria for your staff because you are the employer.

Specific criteria must be met to work in that role. Qualifications may include an educational degree, a certain number of years of experience, and any certifications that an employer believes are required for you to perform successfully in a work capacity. For example, employers often demand a bachelor’s degree, a nursing license, and clinical experience to work as a nurse.

Vision of Job vs Business

A vision is a future plan that directs a firm to attain certain goals. If you own a company, it functions in accordance with your vision. A business allows you to create and achieve goals that will improve your and your workers’ life. You may, for example, have the vision to build an inclusive workplace that delivers safe and inexpensive health goods for customers. Integrating your corporate image with your fundamental beliefs and personal aspirations, you may attain professional happiness and personal accomplishment.

When you work, you contribute to realising someone else’s vision rather than your own. You may work at a job to realise a goal you believe in by looking for a firm whose values connect with yours. If you want to assist in establishing a corporate vision, you may work in management and engage with the CEO. Having a job and not being responsible for developing a corporate vision may also be advantageous. You can concentrate on your objectives and how your employees can assist you in achieving them.

Growth in Career in Job vs Business

Having a business helps you to flourish in a variety of ways. You can enlarge your consumer base or product range and then obtain a physically more prominent place to manage your firm. You may expand by starting another business or opening a new location if you are successful. Professionally, you can consult for other companies or speak at conferences.

In a job, your growth depends on promotions. You can develop professionally by earning certifications and pursuing higher education and other learning opportunities. Your opportunities to grow include making a promotion to management.

Motivation in Job vs Business

Work motivation varies depending on whether you own a firm or work for someone else. For business owners, success and goodwill are common motivators. Developing a brand and expanding your consumer base pushes you to work hard. Earning a profit is also a significant motivator for completing tasks and fulfilling your job obligations to the best of your abilities to succeed.

If you have a job, your employer will utilise your job performance to push you to do better in the future. Raises, promotions, and bonuses are common motivators for employees.

Schedule

Another significant distinction between a company job and a government or corporate position is scheduling freedom. While running a business, you may establish your own schedule, which makes it more flexible but may also require more hours depending on the demands.

Your schedule at work will be determined by your employer. Although there are set working hours, the shifts will vary depending on the firm you work for.

Investment

Starting a business requires a large investment and hence carries more risk than working a job. Aside from a huge quantity of wealth, various types of investments exist.

Finding work requires a lot lesser investment. You must invest in your education to obtain the necessary abilities for a solid corporate career.

Advantages of Business

Independence

Being a business owner means you are the only boss. You have the freedom of making decisions which are crucial for business success.

Lifestyle

Having a business also provides certain lifestyle advantages as you’re in charge, you decide when and where you want to work.

Learning opportunities

A business owner is involved in all aspects of your business. This situation creates numerous opportunities to gain a thorough understanding of the various business functions.

Financial Reward

Despite financial risk, running your own business provides you a chance to make more money than if you were employed by someone else.

Creativity

In business, you’ll be able to work in a field that has expertise. You’ll be able to put your skills and knowledge to use, and you’ll gain personal satisfaction from implementing your ideas.

The Advantages of a Job

Pursuing a job rather than launching a business might provide several advantages that you can enjoy right away when beginning a career. People prefer to work in a job rather than establish a business for a variety of reasons, many of which are related to the rewards of working. Consider the following advantages:

Financial security

From a steady monthly wage to other benefits such as insurance and bonuses, you will have consistent earnings with a job, reducing the likelihood of a financial crisis.

Opportunity

Working in a work role may provide you with the opportunity to enhance your talents and contribute to the achievement of corporate goals. Throughout your work, you may have the opportunity to advance and take on additional tasks or get promoted. Advancement within a firm or career may keep your employment fresh and enjoyable.

Various employment options

When you work, you may quickly switch jobs if you acquire better job positions and offers. While working, you will be exposed to the organisational structure and diversified working environment of corporate life, which will add to your entire personality.

Less accountability

Many people choose to work as an employee rather than run a business since it is less stressful and has fewer obligations. You are exclusively accountable for your achievements and work responsibilities as an employee. This can help you achieve a better work-life balance and focus on other concerns rather than the company where you work.

Flexibility

Because you do not own the firm, you must commit all your time to it. You can work according to the schedule and spend your leisure time doing anything you desire.

Challenges Faced in Jobs

Here are some of the primary obstacles that full-time workers encounter.

High Level of Competition

In most jobs, there is tremendous rivalry for every advancement available. To get a promotion and advance in your career, you will need to put in a lot of work and be at your best all of the time.

The scope of additional financial benefits is limited

A job provides no opportunity for profit, and your monthly payment will be set. Other than a handful of annual bonuses or incentives for outstanding performance, there is little opportunity to receive further financial rewards.

Politics in office

Office politics is another unpleasant feature that can break the tranquillity of professional employment. Rules may also be overly stringent. Working in a job entails adhering to regulations that must be observed to stay in the firm. Even if you disagree with the rules, you must always obey and accept them.

Advantages of business

The following is the list of benefits that committing to being a businessperson is deemed to carry.

Independence

When you own your own business, you will be your own boss. You will be free to make your own judgments and will not be required to respond to anybody. It also eliminates the anxiety of losing your work and promotes job stability.

Flexibility

Many people like to operate a business since it provides them with more freedom. You have control over your working hours and how much you work. This is a major benefit of owning a business and may help you achieve a work-life balance. It is critical to balance your career and personal lives in order to achieve total satisfaction.

Professional Development

As the owner, your duties will be spread throughout several departments. You may learn about marketing, budgeting, and even business economics, which will boost your general abilities and business ethics.

Always be learning, read anything related to your industry!

Challenges Faced in Businesses

Some of the challenges faced by a businessperson are as follows:

Funding

The most complex and first obstacle you will encounter when beginning your business is raising finances to invest in it. Furthermore, there is a chance of losing money early, making it unpredictable.

Competition

Every industry nowadays is riddled with rivals. Whatever type of firm or business you establish, you will undoubtedly encounter stiff competition for clients. You will be under intense pressure to develop novel strategies to captivate potential consumers.

Risky

Running your own business entails a significant amount of risk. While there is the potential for massive profits, there is also the risk of massive losses. There is a chance that you will lose all of your money, time, and effort.

Stress

Running your own business may be a very stressful affair. Aside from managing everything from your staff to day-to-day business operations, you will also be responsible for maintaining income.

FAQs

Q: Are entrepreneurs happier than employees?

Answer: Science claims that, on average, business owners are happier and healthier than employees, however some entrepreneurs may experience the stress of starting a new company.

Q: Is starting a business the only path to financial success?

Answer: Starting your own business can make you wealthy, and not just financially. But it’s not the only path to prosperity, and starting your own business is by no means a surefire method to get wealthy.

Q: What exactly is a job?

Answer: Job is classified as either part-time or full-time labour or employment. It is easily identified as a responsibility or obligation for a certain type of task.

Q: What exactly is a business?

Answer: A business is a group of two or more individuals who work together to achieve a similar purpose. It could be one person, and a business organisation might be profit- or non-profit-oriented.

Conclusion

When making a decision about jobs vs business, evaluating the advantages and disadvantages is critical. To make the best selection, you must consider everything from your interests and skills to your personal and professional goals.

Building a business for purpose will give you tremendous satisfaction, you can build a business for ‘money’ and that’s fine, but the reward is purpose – you want to enjoy the thing you invest most of your life in, therefore would you like to have fun whilst working?

The short answer is you’ll always need more than you budget. There will be curve balls, you’ll be so driven by the idea you’ll be an overnight success, yet, this is rarely the case. My budgeting advice: take your time, and look for any quick wins.

For founders, entrepreneurs and those investing in start-up businesses, it can be difficult to budget effectively. Success doesn’t happen overnight, and often there are unforeseen challenges when budgeting. This blog is intended to provide advice and guidance on budgeting for those in the start-up community. I’ll give you practical tips on how to budget and how to look for quick wins. With this advice, you can improve your financial outlook and stay on track for your long-term goals. Read on for valuable advice on budgeting for start-ups!

First, take a close look at your business model and identify any areas where you can save money. Are there any areas of your business that are needlessly expensive? Can you cut costs in any areas without affecting the quality of your product or service? Reducing your expenses is a great way to improve your bottom line and free up cash for other purposes.

Next, look for any quick wins that can help your business achieve its financial goals. A quick win is a small, easily achievable goal that can have a big impact on your business. For example, if you’re trying to increase sales, a quick win might be to offer a discount on your product. By achieving quick wins, you can stay motivated and focused on your long-term goal of growing your business.

Since you have no past financial data to go on, you must create the budget using your best guess on income and expenses (otherwise known as a profit and loss statement). Before you begin, consider why you need to spend the time to create a budget. Even if you don’t need bank financing, creating a budget is still a valuable exercise for any new and continuing business.

Key Takeaways

A budget is a key component of your startup business plan.

The most difficult part of creating a budget for a new business is estimating your sales.

You should start by calculating your “day one” costs—the expenses needed to open your physical or virtual doors and begin accepting customers.

Next up is calculating your fixed and variable costs and your estimated monthly sales.

Creating a cash-flow statement is also an important part of creating your new business budget.

Questions to Ask Before You Begin Your Budget

Some questions to ask yourself before you begin creating your start-up business budget:

What do you need to open the doors of your business on the first day?

What will your fixed and variable costs be on a continuing basis?

What can you contribute to keep costs low?

What can you get as donations from friends and relatives?

What can you do without?

Note

Keep your “must-haves” to the minimum. The less you need for your business startup, the sooner you can start making a profit.

Step 1: Plan for “Day One” of Your Business Startup

Begin by determining what you will need on “day one” of your business—the costs necessary to open the doors (or to take your website live) and begin accepting customers.

A “day one” start-up budget can be broken down into four categories (depending on your situation, some of the categories may not apply to your business.) The categories are:

Facilities Costs

Facilities costs include all the costs of setting up a leased or purchased location for your store, office, warehouse, or other building. These costs may be called leasehold improvements or tenant improvements. For example, you may need walls or a bathroom or a special secure area in your office or building.

If you are working from home, you probably won’t have location costs but you may have costs to fix up a room in your home for an office or a small production area in your garage.

Facilities costs also include lease security deposits and signage.

Fixed Assets

What are the fixed assets (sometimes called capital expenditures) such as furniture, equipment, and vehicles needed to set up your location and start your business? Fixed assets also include computers and machinery, furniture, and anything for your office, store, or warehouse that is needed to set up your business.

Materials and Supplies

Different from assets, materials and supplies include office supplies and any advertising and promotion materials. You will need an initial supply of these to get started.

Other Miscellaneous Costs

Miscellaneous costs include the initial fees to an accountant to help you set up your accounting system, local licenses and permits, insurance deposits, and legal fees to register your business with government entities (like your state) and prepare operating documents.

In your listing of these startup costs, include items you are contributing to the business, like a computer and office furniture. Note the cost of these items in your list so you can get credit for them as collateral for a business loan.

Step 2: Estimate Monthly Fixed and Variable Expenses

Fixed Expenses

Fixed expenses are costs that don’t change and aren’t dependent on the number of customers you have.Gather information on your fixed expenses each month. Some of the most common monthly fixed expenses include:

Rent

Utilities

Phones (business phones and cell phones)

Credit card processing—monthly fees (transaction fees are variable)

Website service fees

Equipment lease payments

Office supplies

Dues and subscriptions to professional publications

Advertising, publicity, and promotion commitments, like social media or continuing online ads

Business insurance

Professional fees (legal and accounting)

Employee pay/benefits. (This category is semi-fixed, because you may be able to lower your employee costs at times.)

Miscellaneous expenses

Business loan payment

Variable Expenses

Variable expenses are expenses that will change with the number of customers you work with every month. These might include:

Postage, mailing, packaging, and shipping costs

Commissions on sales

Production costs

Raw materials

The wholesale price of goods to be re-sold

If you have a service business, you may not need many variable expenses.

Step 3: Estimate Monthly Sales

Estimating your profits and sales is probably the most difficult part of a budget because, for a new company, you don’t have a track record on which to base your estimate. You might want to do three different sales projections:

Best-case scenario, in which you show your most optimistic estimate for first-year sales.

Worst-case scenario, in which you show your least optimistic scenario, with very little sales during the first six months to a year.

Likely scenario, somewhere in between. The likely scenario would be the one to show your lender.

To be realistic in your budgeting, you must assume that not all sales will be collected. Depending on the type of business you have and the way customers pay, you might have a greater or smaller collections percentage.

Include a collections percentage along with your estimate of sales for each month. For example, if you estimate sales in month one to be $50,000 and your collection percentage is 85%, show your cash for the month to be $42,500.

Calculate the variable costs of sales for each month based on sales for the month. For example, if your estimated sales for a month are 2,500 units and your variable costs are $5.50 per unit, total variable costs for the month would be $13,750.

Add monthly variable costs to monthly fixed costs to get total monthly costs (expenses).

Note

If you are selling products, you might want to calculate your break-even point to include with your budget. The break-even point shows when you will start making a profit on each sale.

Step 4: Create a Cash-Flow Statement

Cash flow is literally the amount of money going into and out of your business each month.

Begin your cash flow statement by combining total costs with total collections of money from all sales for each month. Remember that sales and collections might be different, unless you have a cash or credit business. For the cash flow statement, you’ll need to use collections.

The monthly cash flow totals should look something like this:

Monthly sales $50,000

Collected $42,500

Total fixed costs $26,900

Total variable costs $13,750

Total cash balance $2,150

The $2,150 represents your total cash balance for the month, not your profit.

By changing your sales figures using the three scenarios above, you can see the result in your cash balance at the end of each month. This cash balance can give you information about your cash needs and how much you might need to borrow for working capital.

Note

Managing your cash flow is a key tool for keeping your new business afloat. And cash flow is more important than profits. You can be making a profit on paper, but if you don’t have money in the bank, your business won’t be able to pay its bills.

Tips for Creating Your Business Startup Budget

Use youraccounting software program to create your budget, so you can use existing accounts and make changes more easily. If you don’t have an accounting software program, you can use a spreadsheet program.

Most lenders require three years of cash flow statements on a month-by-month basis, and three years of quarterly and annual income statements (P&Ls).

Income taxes are a variable expense, and you don’t know what taxes you will have to pay until you calculate your net income. Don’t include taxes in fixed expenses or variable expenses but make these a separate category.

Note

Estimate sales LOW and expenses HIGH. Everything always costs more and takes longer than you think it will, and it will take longer to get sales going than you think it will.

Frequently Asked Questions

What are the four steps to creating a budget for your small business?

One: Calculating your “day one” costs: the expenses absolutely necessary to open your business and begin accepting customers. Two: Estimating your monthly fixed and variable expenses. Three: Estimating monthly revenue. Four: Create a cash-flow statement.

What are the most common expenses for small businesses?

Some of the most common monthly fixed expenses for small businesses and start-ups include rent, utilities, equipment, website service fees, insurance, and labor. Common variable expenses include packaging, production, and shipping costs, sales commissions, and raw materials.

Each business (sector agnostic) will use this framework, for a structured plan, let’s discover if we can work together.